If you like numbers, this one is for you!

Editor's note: After this article was published, additional information was realized, which called for a correction. That correction was included in the December 11, 2025, issue which can be accessed here: Correction concerning Mason Co. BESS projects | The Menard News and Messenger

By Collyn Wright

In researching the tax implications for the proposed BESS facility in Menard, I learned their taxable value is set by the public utilities commission based on megawatt (MW) output and is assessed by the Mineral, Industrial, and Utility Appraisers contracted to appraise those values within the county, as is standard practice throughout the state. The local chief appraiser for the counties are not responsible for setting the taxable value for utilities, including BESS facilities. It is industry standard for a project developer to request a tax abatement or discount from taxing entities. For low socioeconomic counties, tax abatements are often granted by a taxing entity to entice a project to choose their county for the project and income infusion over another location. Tax abatements can be used to reduce the taxes paid by the entity for a maximum of 10 years and/or as a tool to freeze the taxable value of a project, even if the rest of the taxable value schedules for the county change for the period of 10 years. State law prohibits an abatement for school districts and hospital districts, meaning those entities will receive the full taxable value per $100 regardless of a tax abatement possibly granted.

I recently reached out to the Chief Appraiser in Mason to get information on the active BESS site, Bat Cave Energy Storage, LLC, and its value to their tax roll. What I found is that the battery storage facility in Mason provides the most taxable value out of all properties and utilities currently taxed within Mason County. While the Mason facility has its downfalls, the tax revenue provided to the county is not one of them.

The Bat Cave facility is understandably controversial due to its placement within in 60ft of a residence. The fan noise, to cool the batteries in this particular installment, is an audible nuisance for the property owners within close proximity; as is the concern for fire, if the safety mechanisms built into the facility were to fail. The property owner most affected by this careless installation, reportedly has their house on the market to sell, but has been unable to do so with the BESS project so close to their back yard.

In contrast, the company chosen for the proposed battery storage facility in Menard, RES, does not allow their facilities to be built within 1,000 ft of a structure or dwelling. The proposed battery storage facility in Menard County, Black and Gold, is actually planned to be built farther than 1,500 feet from structures. The property surrounding the proposed BESS facility in Menard County is owned and will continue to be owned by the property owner entertaining the idea of selling the small portion of their acreage for the facility. The Black and Gold project will only border the current landowner. Deed restrictions will also be put in place to limit future use after the functional life of the facility has been reached and the site is decommissioned using the funds from the state mandated posted bond.

When looking at the tax revenue, it is important to note the Bat Cave Energy Storage, LLC project is being taxed as a 100MW facility, with the proposed Menard facility being between 100MW and 200MW. An abatement was not granted for the county or water district portion of the property taxes in Mason.

Bat Cave began paying taxes in Mason County for the 2021 tax year in January of 2022 for a total taxable value during the construction phase as $10,443,410. During 2021 the Water District’s tax rate was $.03200 levying $3,341.89. Mason ISD’s tax rate was $1.11370 generating a tax bill to the school district of $116,308.25. Mason County’s tax rate was $.61019 garnering $63,724.54 for the county. The total tax payment for the 2021 taxable value for Bat Cave Energy Storage, LLC was $183,374.68.

In Jan of 2022 the construction was complete and the taxable value for the same project was $40,500,000. The Water District’s rate was $.03035 bringing in $12,291.75. MISD’s rate was $1.11370 levying $451,048.50. The county’s rate was $.61019 for a $247,126.55. Total taxes paid by Bat Cave- $710,466.80.

2023 is the first year on record for depreciation, the taxable value was $37,800.000. The Water District’s rate was $.03030 for $11,453.40 in tax revenue. Mason ISD’s rate was $1.11370 bringing their revenue from the project to $420,978.60. The County was at $.60070 for $227,064.50. The project’s total tax payment was $659,496.60.

In 2024, the taxable value was $34,633,720. Water District rate: $.02976 for a total of $10,307.69. Mason ISD rate: $1.10800 for a total of $383,741.62. County $.64270 for a total of $222,590.92. Total $616,640.23. While the facility will continue to depreciate, the taxable value will never go below $8,100,000 or 20% of the highest taxable value. At this time, the property tax schedules of value for properties in Mason County have not been adjusted due to the installation of the battery storage facility. The total of tax payments added to the county’s coffers are $2,169,977.21 since the project began construction in 2021.

The next closet county with running BESS facilities is in Kimble County. In speaking with the Kimble County Chief Tax Appraiser, I learned there is one 10MW BESS facility and another 9MW facility is under construction and will be operational in 2026.

HEN Infrastructure, LLC in Kimble County received their first tax bill for the 2023 tax year, for a taxable value of $4,515,970. A tax abatement was not requested for the project; therefore, many citizens have no idea there is an operational facility in town. There have been zero problems with the current facility. The tax roll saw an increase last year for the first time when the facility was added. Junction ISD’s rate was $.6692000 for a payment of $30,220.87. Kimble County’s rate was $.4589000 garnering a $20,723.79 check. The Kimble County Hospital District rate was $.3226000 for a payment of $14,568.52. The last Kimble County taxing unit to receive funding from the project for the 2023 year was Kimble County Groundwater at a rate of $.0076000 for $343.21. The total tax bill levied for the HEN project was $65,856.39 for the year.

For the 2024 tax year, the total taxable value of the HEN BESS project was $4,215,000 with a tax bill of $59,730.02. Junction ISD’s tax rate was set at $.6618000 for $27,894.87. Kimble County adopted a tax rate for 2024 of $.4364820 for $18,397.72 of income payable to the county. The Kimble County Hospital District rate was set at $.311000 for $13,108.66. Kimble County Groundwater rate was $.0078000 for $328.77.

The tax rates for the 2nd planned storage facility should be comparable to current facility given the similarities in megawatt output. Each of the Kimble County facilities are approximately 1/10th to 1/20th the size of the proposed Menard County facility.

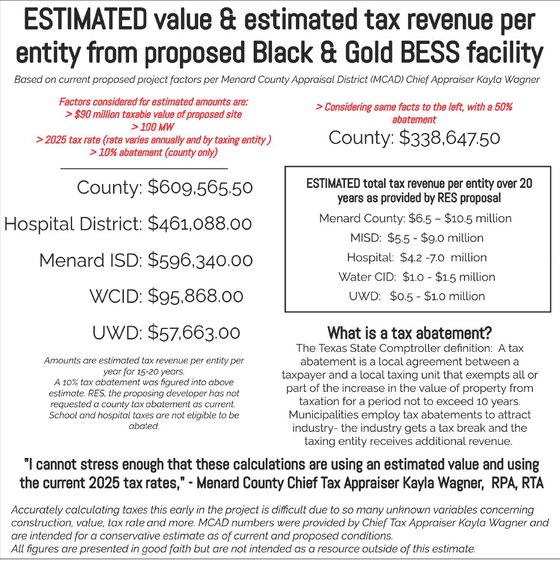

It is impossible to predict future tax levies for each taxing entity within a county (any county) because new tax rates are adopted each year. The taxable value of the asset will depreciate each year over its expected 20-year project life, but the taxable value will not go below 20% of the original fully taxable value. Using this year’s rates for each taxing entity in Menard County with a range for the proposed facility’s megawatt capacity, an approximate range for potential income can be projected for 1 year. The current tax rates listed per $100 on the Menard CAD 2025 Tax Statements are: County .75255000, Hospital District .51232000, Menard ISD .66260000, Underground Water District .06407000, Flood Control and Lateral Roads .0077200, and Water Improvement District .106520000.